EMB Newsletter July/August 2020

Newsletter as PDF

Contact

EMB - European Milk Board asbl

Rue de la Loi 155

B-1040 Bruxelles

Phone: +32 - 2808 - 1935

Fax: +32 - 2808 - 8265

Dear dairy farmers, dear interested parties,

Over the last few days and weeks, many have added their voices to the chorus of those who see a recovery on the milk market. If you were to listen to dairies and processors, you would think that everything is back on track. Farmers’ associations, retailers and a broad range of policy-makers are singing along to this hopeful tune. Are we from the EMB just inciting panic?

It would seem that the opening of private storage has solved all the world’s problems. The agricultural press is talking about a “noticeable recovery” and “positive trends”. Some fellow farmers do, in fact, believe that yet another ‘competitor’ going out of business is a positive trend, and are dutifully keeping their production going as usual. And, thankfully, we can travel again. So, we farmers will not have to reschedule our two to three weeks of well-earned time off.

It surprises me to see that people think that dairy farmers can be so quickly and easily calmed down. All you need to do is look at the milk price. In many places, it is already below the 30-cent threshold – which is also psychologically very important – and this in the face of total production costs amounting to almost 45 cents. Stocks in warehouses are growing every week and exert additional downward pressure on the price. In some countries, the quotas for cheese were entirely filled in the first few weeks. If all of this was not enough, too many farms are suffering major liquidity crunches. Most of them are merely one step away from heading to the bank – that is, if new loans are even being granted. Even though all of this sounds like anything but “recovery”, the chorus of appeasement is only growing.

But we at the EMB are going to continue to make our position heard – loud and clear. As long as prices are in a downward spiral, with production continuing full-steam ahead nonetheless, and there is no effective crisis instrument at EU level, nothing is really on track. When the imbalance is as grave as the current situation, a reduction in milk volume is the only way to bring some relief. Together with our 21 member organisations from 16 countries, we stand united behind this message. Inciting panic is far removed from our intent. With our Market Responsibility Programme, we are ready to make a constructive contribution to the debate towards finding an effective solution. It is quite clear that unless production is reduced, the current issues will persist for a long time and one dairy farm after the other will be driven into the ground.

As the EMB, we stand in solidarity with all European dairy farmers. In the context of the European Commission’s new sustainability strategy, we must preserve our family farms – each and every one counts. But this survival hinges on producer prices that cover our production costs in full and allow us to draw a decent income. Sustainable farming is only possible if it encompasses the well-being of farmers, consumers and society.

But if our message falls on deaf ears, perhaps we will, once again, need to make ourselves heard in Brussels in the near future. Speaking of travel, the EU capital has always been just a tractor-ride away!

Erwin Schöpges, President of the European Milk Board (EMB)

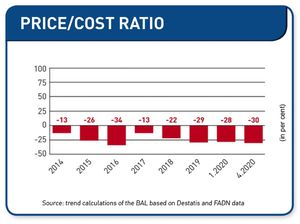

Price/cost ratio in Germany almost at 2016 crisis level

- @ EMB / BAL

The latest results of the study on milk production costs in Germany show a clear shortfall, with milk producers missing 30% to cover their cost of production. Current figures of April 2020 show that the cost of production amounts to 46.76 ct/kg, whereas the farm-gate milk price was only 32.68 ct/kg in the same period. Producers thus lack 14.08 ct/kg to cover their costs. These figures come from the quarterly cost study published by the BAL (Büro für Agrarsoziologie und Landwirtschaft, German farm economics and rural sociology office). With the figures for April 2020, the calculation of milk production costs was adapted to the latest FADN data of 2018.

The milk production costs of almost 47 cents/kg on average are mainly due to the effects of the dry years since 2018. As in the years 2012/2013, cost developments and a weak farm-gate milk price below 33 cents/kg are now leading to a producer price crisis. The price/cost ratio almost reaches the 2016 crisis level.

Development of milk production costs in Germany

This is the evolution of milk production costs in Germany from 2014 to April 2020.

Price/cost ratio (shortfall)

The price/cost ratio illustrates to which extent milk prices cover the cost of production. In April 2020, producers only recovered 70% of their production costs from the milk price; the shortfall was thus 30%.

Here you see the cost shortfall since 2014.

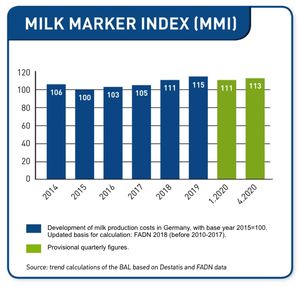

Milk Marker Index – MMI

The Milk Marker Index (MMI) represents the evolution of milk production costs. In April 2020, the MMI was at 113, i.e. production costs for German dairy farmers had risen by 13% as compared to the base year 2015 (2015=100).

Here you see the evolution of the Milk Marker Index over time.

New: study on organic milk production costs

In November 2019, a study on the cost of producing organic milk in Germany was published (period: 2011 to the most recent milk year). You can find this study here (in German, English version available soon).

Study on milk production costs in six key milk producing countries

Cost calculations are regularly carried out in Germany but also in five other countries. They also show very clearly that the prices paid to milk producers do not cover the cost of production. The study on milk production costs in Belgium, Denmark, France, Germany, Luxembourg and the Netherlands in 2017 is available here. In a short video you can see all figures at a glance.

Chronic production cost shortfall – what is the solution?

The European Milk Board promotes a legally anchored crisis instrument to counteract the chronic shortfall between production costs and milk prices. The Market Responsibility Programme (MRP) observes and reacts to market signals by aligning production.

Here you have a short description of the EMB's Market Responsibility Programme.

Background:

Commissioned by the European Milk Board and Germany's MEG Milch Board, the BAL (Büro für Agrarsoziologie und Landwirtschaft, Farm economics and rural sociology office) started compiling comprehensive data on milk production costs in Germany in 2012 for the study entitled "What is the cost of producing milk?". The calculation is based on data from the EU Farm Accountancy Data Network (FADN) as well as the German Federal Statistical Office (Destatis), and has been updated every quarter since 2014.

Download fact sheet.

EMB press release of 15 July 2020

In search of courageous ministers: the crisis on the dairy market is getting worse, but policy-makers look on passively

- © Astrid Sauvage

The situation on the dairy market continues to be tense. While demand has decreased due to the coronavirus crisis, EU-wide supply has increased by 2.8% as compared to the same period last year. This is further compounded by the current seasonal peak in milk supply.

Though demand from wholesale customers and restaurants has increased marginally again, the collapse of exports continues to be an issue. As a result, many German dairies have reduced farm-gate prices, and further reductions have been announced for the recently concluded month of May. In some areas, the milk price has already fallen below the psychologically important threshold of 30 cents. These excessively low prices are coinciding in many areas with feed shortages due to yet another drought.

In other EU Member States, the milk price has also sunk by 9% across the board as compared to the previous month. It is especially low at about 28 cents in the Baltic region, Belgium and Ireland. The mitigating measure of private storage adopted by the EU is being taken up, though some countries have already filled their allowed quotas for cheese. In France, dairy farmers who reduce their production by a small percentage receive 32 cents as compensation (editor's note: for every litre of milk not produced) from the fund worth 10 million euros set up by the national interbranch organisation. Some Austrian dairies are using internal incentive systems to encourage volume reduction. The possibility of volume planning within producer organisations approved by the European Commission is, however, not being taken up. Germany is not using this option either, even though numerous local milk producer organisations and dairies had called for a reduction in milk volumes. This shows that measures at individual company level are very unpopular when no nationwide funded compensation is provided and comprehensive – ideally EU-wide – coordination is missing.

Disappointing Agriculture Ministers’ Conference

Many dairy farmers had hoped that the conference of the German federal states’ agriculture ministers on 8 May would lead to some progress. It was an opportunity to reduce distortions on the dairy market and reinstate market balance by adopting decisions for volume reduction, as was done in previous years. Joint appeals by farmer representatives from different associations for such action fell on deaf ears. However, the ministers unanimously welcomed and supported the EU decision to promote private storage and called on the sector to use the 2030 Sector Strategy to bring stability, even though this programme does not have any suitable instruments to do so. The fact that conservative (CDU) and liberal (FDP) ministers are unwilling to lift a finger to stabilise the market comes as no big surprise. But to see that social-democratic (SPD) farm ministers are doing nothing to improve the income situation of farmers – though they have suddenly developed a soft spot for harvesters and abattoir workers – is a definite disappointment. To see that many agriculture ministers from the Greens have completely abandoned their earlier, clear support for regulation measures during dairy market crises is like a slap in the face. We are lacking courageous ministers like Brunner, Meyer and Habeck who filled these positions a few years ago. At the conference, their incumbent colleagues basically positioned themselves against farmers and in favour of the food industry. This is further encouragement for Federal Agriculture Minister Klöckner to passively look on. Farmer representatives, who are already actively promoting volume discipline, must now be even more effective in keeping up the pressure. Societal support like that for the common declaration by AbL and BUND on World Milk Day will be indispensable.

Extract from an article by Ottmar Ilchmann, Chairman of the AbL in the federal state of Lower Saxony, published in “Bauerstimme” farmers’ magazine on 12 June 2020

Trial of origin labelling for milk and meat extended to the end of 2021

- © Pixabay

Launched in 2016, the trial of origin labelling for meat and milk in processed products in France has been extended once again till the end of 2021. This decree makes origin labelling compulsory for the milk and meat used as ingredients in pre-packed food products.

Coordination Rurale, who advocates for comprehensive traceability of all ingredients in agro-food products, believes that this kind of transparency is indispensable for consumers to have all the information they need to choose a product that lives up to their expectations. Therefore, Coordination Rurale (CR) raised awareness among consumers during the 2018 and 2019 editions of the International Agriculture Fair with its ‘shopping cart of non-traceability’.

A trial that does not go all the way

Current European legislation for origin labelling is not comprehensive enough and too lax because it only looks at certain products – fresh fruit and vegetables, wine, milk and meat. With respect to milk, the decree underpinning this trial is only applicable if the total weight of the ingredient is 50% of the final product. In other terms, if the amount of milk used as an ingredient only corresponds to 49% of the product's total weight, the manufacturer is not obliged to state the origin of the milk used. Such a high threshold means that a wide range of products automatically fall outside the scope of this decree. According to Coordination Rurale, this threshold is too high and all products, with no exception, should be labelled with the origin of the ingredients used, be it fresh or processed, without any thresholds.

Need to launch this process at European level

Compulsory origin labelling for foodstuffs makes it possible to avoid abusive trading practices and fraud by certain manufacturers. Such illegal behaviour sometimes leads to food scandals that threaten public health and destroy the confidence of consumers, who are increasingly mistrustful when it comes to food. Therefore, it is absolutely essential for the name of the country of origin to be mentioned on labels, and for indications like “EU”, “non-EU” and “EU and non-EU” to be banned.

In spite of its shortcomings, this trial in France shows that it is possible to put such a system in place, contrary to claims from the food industry who have always opposed this measure and continue to do so. With respect to the trial itself, CR hopes that it shall be implemented by the European Union for all products that include agricultural foodstuffs (milk, meat as well as food grains, fruits, vegetables etc.). The food industry must stop their hypocritical narrative where they hail the excellent quality of our raw agricultural products and ride piggyback on our image, while at the same time, they do all they can to buy them as cheaply as possible for their processed products.

Sophie Lenaerts, head of the milk section at Coordination Rurale (CR)

Latest information from Germany

- © EMB

The deadline for applications for private storage aid expired on 30 June 2020. Private storage was barely used for cheese in Germany: at the end of June 2020, dairies were holding only 901 tonnes of state-subsidised cheese in their warehouses. There was a long way to go before filling the quota of 21,726 tonnes allocated to Germany. Private storage was used to a larger extent for butter at 13,368 tonnes and for skimmed milk powder at 10,025 tonnes.

The German Farmers’ Association (DBV) and the interest group of cooperative milk processors (IGM) stated in a joint press release that the sector had cooperated constructively! There are wide-ranging assumptions underpinning the hesitant uptake of private storage in Germany. One of them is that this measure is being consciously under-utilised in order to stifle any and all further discussion about additional market measures (volume reduction).

Spot markets recover significantly

In early/mid-May 2020, the price of freely-traded milk or milk concentrate was quoted at 21/22 cents per kg. An increase of about 10 cents per kg was announced four weeks later, with all freely-traded milk/milk concentrate immediately taken up and drained from the market. Dairies with available capacity to produce butter, milk powder and cheese massively bought cheap raw materials from the spot market. They were clearly hoping for ‘speculation gains’ but at whose cost? The answer is quite simple: at the cost of dairy farmers, who produced the milk that dairies are offloading at throw-away prices!

IGM – the faces behind the name

In early 2017, unsalaried representatives from six large cooperative dairies came together as IGM, with a seventh joining their ranks in the meantime. This platform includes Arla Foods amba, Bayerische Milchindustrie (BMI) eG, Deutsches Milchkontor (DMK) eG, Hochwald EG, Molkerei Ammerland eG, Royal FrieslandCampina UA and Uelzena EG. All IGM representatives hold high-ranking positions in their respective dairies, making IGM yet another organisation in the fairway of the German cooperative association. The glimmer of hope nurtured by former Federal Minister for Agriculture Christian Schmidt that the creation of IGM would lead to the founding of an interbranch organisation did not come to be – the interests of the dairy companies regrouped in IGM seem to be too heterogeneous.

Producer prices drop further

Milk prices for May will be an average 2 cents/kg lower than the previous month, somewhere between 27 cents/kg and 36 cents/kg (base price/net). The number of dairies that are paying prices below the 30-cent threshold is rising significantly. The 36-cent dairy enjoys an excellent market position; the coverage area, however, is the alpine region. One dairy has already announced a farm-gate price of 25 cents/kg for June. The milk price is currently evolving contrary to the market optimism and reassurances proclaimed by the German Farmers’ Association (DBV) and the dairy sector’s organisations.

Johannes Fritz, Bundesverband Deutscher Milchviehhalter e. V.(BDM)

Nitrates Directive: information from countries

- © Myriam Zilles, Pixabay

We continue our series on the Nitrates Directive with reports from Belgium and Germany. The Belgian contribution explains the fertiliser restrictions and application periods. From Germany, we have an overview of the main changes to the amended Fertiliser Ordinance that came into force on 1 May.

Fertiliser policy in Belgium

The Nitrates Directive has been implemented in Wallonia through the Programme for Sustainable Management of Nitrogen in Agriculture (Programme de Gestion Durable de l'Azote en Agriculture, PGDA), where the third action plan has been in force since 15 June 2014. In order to reduce the pollution of ground and surface waters caused by nitrates from agriculture, the Nitrates Directive foresees a revision of the PGDA every four years.

Maximum application thresholds

On grassland: The maximum average amount of organic nitrogen that can be applied on grassland is 230 kg per hectare per year. The return of nitrogen to the soil by animals at pasture is factored in when calculating organic and total nitrogen input. The maximum total nitrogen input (organic + mineral) is 350 kg per hectare per year.

On arable land: With crop rotation (2-5 years), the maximum average amount of organic nitrogen that can be applied on arable land is 115 kg per hectare per year. For every plot, a maximum 230 kg/ha of organic nitrogen can be applied. The maximum total nitrogen input (organic + mineral) is 250 kg per hectare per year.

In vulnerable zones: In vulnerable zones, the average amount of organic nitrogen added per hectare for the farm as a whole (arable land and grassland) cannot surpass 170 kg/ha.

Application periods

Application periods are authorised on the basis of type of farmyard manure used, location of the plot (in a vulnerable zone or not), and on land use (arable land or grassland). Since 1 January 2015, the application of slurry “by spraying it from as spreader” (non-inverted splash plate) using tankers with a capacity of more than 10,000 litres is prohibited.

Since 2008, all farmers with more than 20% of their land in a vulnerable zone are subject to nitrate concentration testing for their plots. This concentration is calculated by measuring potential nitrogen leaching. The potential nitrogen leaching refers to the remaining nitrates still present in the soil after the harvest in autumn. This value is monitored and used as a tool to ensure good nitrogen management in vulnerable zones.

Source: PROTECT'eau asbl

Germany – key changes in the new Fertiliser Ordinance

The Bundesrat adopted the new Fertiliser Ordinance in late March, and it came into force on 1 May 2020. We shall now look at the main changes that have been introduced.

- No more nutrient comparison for nitrogen (N) and phosphate (P). Instead of the established compulsory nutrient comparison, an accurate and prompt account of the amount of fertiliser (mineral, organic) actually applied will now have to be provided.

- Application of liquid organic manure on grassland and arable land with multi-year field forage cropping sown by 15 May is limited to 80 kg total N/ha in the period between 1 September and the start of the closed period.

- The closed period for solid manure from ungulates as well as for composts has been extended by two weeks (1 December to 15 January), and a closed period has been introduced for fertilisers containing phosphates (1 December to 15 January).

- Exceeding the originally reported nitrogen fertiliser requirement due to unforeseen circumstances is allowed up to a maximum 10 percent.

- Distance from water bodies without application in areas with a slope of 5 percent and above increased from one metre to three metres and in areas with a slope of 10 percent and above to five metres.

Additional amendments for farms in nitrate vulnerable zones:

- Reduction of fertiliser needs by 20 percent (farm average) of the areas farmed in the NVZs. Field-related nitrogen ceiling of 170 kg per hectare for application of organic and organic-mineral fertilisers.

- Closed period for grassland and land with multi-cut field forage cropping sown by 15 May in NVZs extended by an additional two weeks (1 October to 31 January; currently 15 October to 31 January in Schleswig-Holstein).

- Application of liquid organic manure on grassland and arable land with multi-year field forage cropping sown by 15 May limited to 60 kg total N/ha in the period between 1 September and the start of the closed period.

Bundesverband Deutscher Milchviehhalter e. V. (BDM)

Interview with Adrien Lefèvre, Vice-President of FaireFrance

- © FaireFrance

The crisis triggered by the COVID-19 pandemic has also hit the dairy sector. Adrien Lefèvre, Vice-President of FaireFrance and dairy farmer in the Ardennes, answers some of our questions.

How has the current situation affected the sales of FaireFrance fair milk?

When the confinement was announced, consumers flocked to shops. We were lucky to have an adequate stock of our fair milk products in these same shops. Long-life products like UHT milk and cream were in high demand from customers who, at that point in time, did not know how long this situation would last. Furthermore, FaireFrance products are unique because they are entirely produced in our country, and this was a plus-point for citizens looking to reorient their consumption to local products.

How have FaireFrance sales evolved in this unusual period?

During the confinement, the sales of FaireFrance products increased by 80% as compared to the same period in 2019. There was high demand for semi-skimmed milk in cartons. There was only a slight variation in demand for organic milk. In order to favour the largest productions, we made some strategic choices, most notably by changing our palletisation (half pallets instead of full pallets) and by temporarily discontinuing the production of 50-cl packs.

How are farmers managing to deal with the current exceptional circumstances, in addition to their daily work on the farm?

The farmers who work with the brand and especially our Board members and employees held a number of online crisis management meetings because we are all from different regions and we had to find quick solutions, mainly to solve the difficulties in ensuring that shops were kept supplied.

Of course, the crisis triggered by the pandemic has led to some complications, especially due to sections of the transport sector being put on short-time work programmes and delivery times thus becoming twice as long. Furthermore, issues with some forms of palletisation and certain kinds of packaging also led to products being temporarily out of stock.

At this juncture when there is major uncertainty about milk prices all over Europe, could fair milk be a solution?

Yes, in these exceptional circumstances, fair milk is a veritable crisis management instrument. Farmers working with FaireFrance receive a guaranteed price of 45 cents per litre of milk sold. The significant increase in sales has led to real, additional revenue for our members and has also been the perfect response to the expectations of our consumers and citizens.

Do you think that these “consumers/citizens” will continue to buy FaireFrance’s fair milk products?

We have been pioneers in this field since we began to sell our first packs of milk in 2013, and we have only seen our pool of consumers grow. Our concept is ideal to guarantee fair remuneration to every stakeholder in the sector. It could not be more sustainable. In addition, our initiative responds to the changing consumption behaviour of citizens who prefer to buy local products rather than low-cost products that are often imported. The way I see it, this crisis will only speed up these positive changes in consumption.

Thank you for your input, Mr Lefèvre!

Vanessa Langer, EMB

Swiss dairy farmers are being swindled yet again

- © Pixabay

For the first time in years, Switzerland is facing a major butter shortage. This is because of the increase in cheese production. Even though butter production would lead to a better price for farmers, cheese production offers greater margins for processors.

And after all, it is the processors who have the final say. The Swiss interbranch organisation for milk has now requested to import 1000 tonnes of butter. This has been undertaken with assurances from processors and traders that the price for milk fat shall be raised so that farmers receive a better milk price. However, the milk prices announced for July only show a slight increase in base price. As deductions have also been increased in parallel, a better milk price still remains a pipe dream.

It is quite the paradox: money is taken away from farmers so that cheap domestic butter can be provided to the food industry which, in turn, is exporting Swiss products by the truckload. At customs, these trucks cross paths with those carrying butter imports.

The Swiss farmers’ association is outraged: “The current situation in the dairy industry is unacceptable.” The powerlessness of farmers is even causing tempers to flare in the highest echelons of the Association.

Werner Locher, secretary at BIG-M (Bäuerliche Interessengruppe für Marktkampf)

Impressum

European Milk Board asbl

Rue de la Loi 155

B-1040 Bruxelles

Phone: +32 2808 1935

Fax: +32 2808 8265

E-Mail: office@europeanmilkboard.org

Website: http://www.europeanmilkboard.org